")

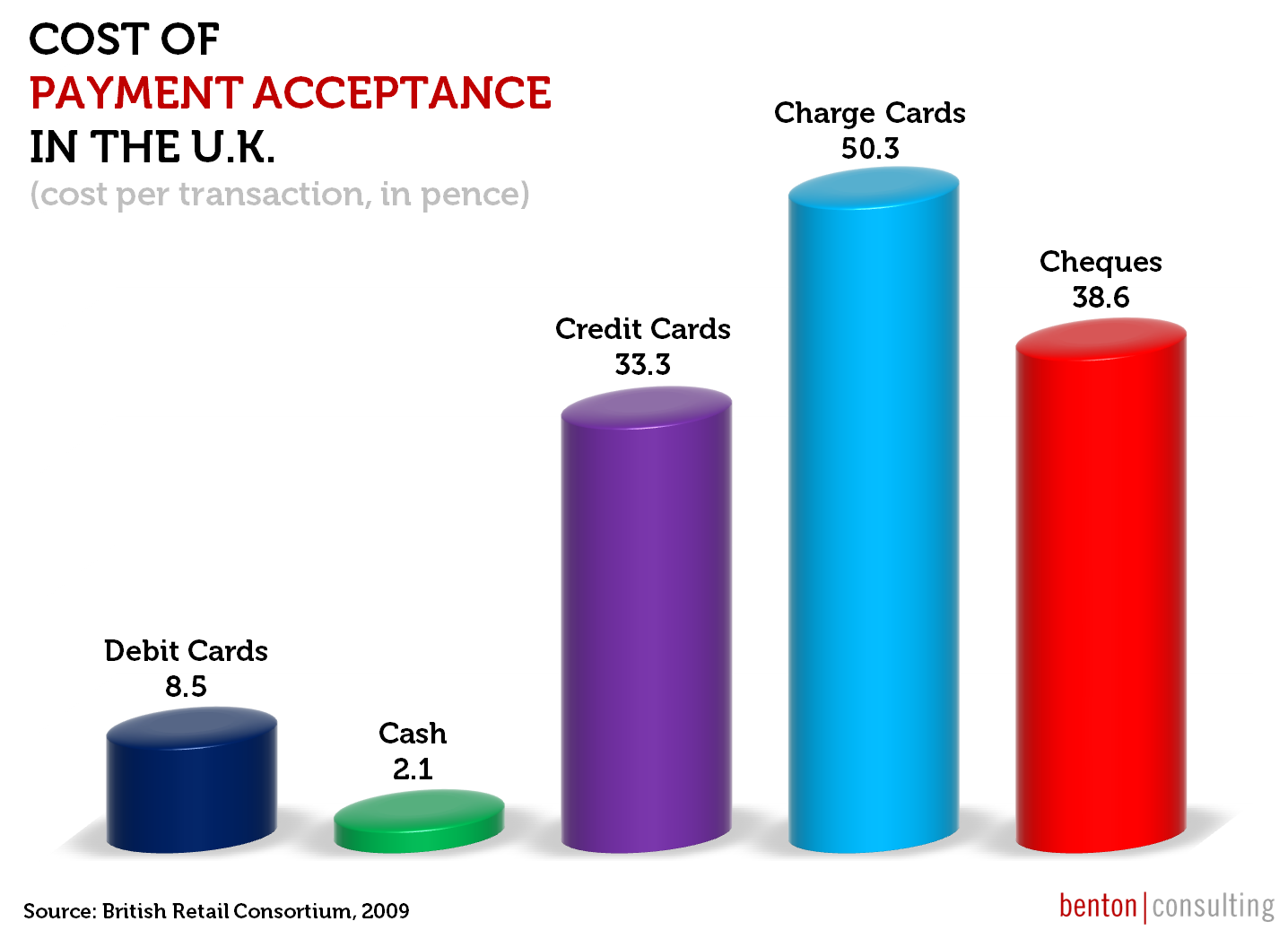

In a report just published by the British Retail Consortium (found here), an analysis of payment acceptance was done to determine the frequency (transaction share and dollar volume share) and cost by payment type.

I’ll be the first to admit that the payment costs in the U.K. are not directly attributable to the U.S. However, given the interest in the Durbin Bill, I did find the Debit cost interesting.

What we know about the debit costs in the U.K. is that they are much lower than the U.S. For arguments sake, let’s say that the U.S. costs are three times higher (a case FOR the Durbin Amendment?). If that is the case, then the U.S. Debit cost is still less than the check (or cheque) costs. Isn’t this what Debit was supposed to supplant? If the cost is less, why such passioned pleas against Debit?

Over the years, I have performed similar studies, and they typically come out the same. Debit is almost always less than the burden cost of checks. The surprising stat is that usually, the cash acceptance cost is on par with Debit. I am not sure of the methodology for this analysis, but that cost seems quite low.

What does all of this mean? To me, it means two things.

First, it means that Debit Interchange may not be as out of control as the retailer would like to think. Interchange is about transfer of value. If the alternative is check, the retailers are getting a better deal.

Second, it means that the methodology used will have a dramatic affect on the outcome. The Durbin amendment puts forth a need to tie Interchange to actual costs incurred. How can this be standardized? Every Issuer has different costs, borne by the systems choices and the scale of the processing. Every Issuer chooses to allocate different cost items to their products.

{kind=link}