A new paper from the Boston Fed was released last week, entitled, “Who Gains and Who Loses from Credit Card Payments? Theory and Calibrations.” For payment systems aficionados, it is important reading. The premise is straightforward: which consumers are the winners and losers when making payment type selection.

The simple conclusion is that cash users subsidize credit card users. Umm… didn’t we know this inherently? When the price of goods is the same for both payors, the one that receives back-end economic benefit must be the winner. What is interesting in this white paper was the lengths undertaken to prove the amount of economic benefit. Specifically:

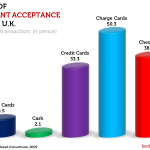

On average, each cash-using household pays $151 to card-using households and each card-using household receives $1,482 from cash users every year.

Yikes! It goes on to ad an income variant to this analysis:

…the lowest-income household ($20,000 or less annually) pays $23 and the highest-income household ($150,000 or more annually) receives $756 every year.

It definitely makes you want to be on the winning side of that equation. But the analysis does skip one important underlying behavior – revolving debt. Obviously, there is a significant cost to revolving debt to the consumer. Economists have long agreed that, in general, debt impacts its society or economy. Financial structures are built to accommodate this. But when looking at the microeconomic impact, as is shown in this paper, that is never truer. In other words, as a card user, my rewards and benefits are being subsidized by cash users. Whether I pocket that whole amount, or apply the economic benefit against or my debt as a subsidy, the cash user is unwittingly helping me.

How does this relate to recent regulation?

Does the passing of the Dodd-Frank Wall Street Reform and Consumer Protection Act improve create a closer equilibrium? Will the reduction of Interchange and processing costs bring the two payors closer to economic equality?

Yes, but not for the reason one thinks. It is my belief that the law will not lower prices. Look at the Australian regulation. The consensus there is that it had no impact on consumer prices.

Therefore, what will happen is that cash and card users will further subsidize retailers:

Cash and card users will pay the same amount

Retailers will have lower costs

Issuers will receive less Interchange

Card user will not receive as many benefits on the back end

So, in this scenario, I went from having the choice of payment type to dictate my economic outcome, to having no choice.

Yipee.

{kind=link}

[…] This post was mentioned on Twitter by Dorado Industries, Benton Consulting. Benton Consulting said: Boston Fed paper: Cash users subsidize Card users – Our opinion at http://bit.ly/9ow3Mw […]

[…] consumers are going to be looking for new products that shift the payments paradigm (though, probably not Cash), or current products that are lower-cost for the banks to provide so that they can still offer them […]